July 23, 2012 (JS Research)

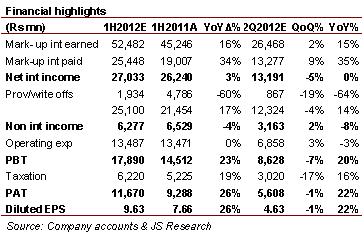

We preview Habib Bank Limited (HBL) 2Q2012 result where the bank is expected to report unconsolidated earnings of Rs5.6bn (EPS Rs4.63), an increase of 22%YoY. However, on a QoQ basis the earnings are likely to see a marginal decline of 1%, mainly on account of lower net interest income. Cumulative 1H2012 earnings are anticipated to jump by 26%YoY to Rs11.7bn (EPS Rs9.63). This significant growth will be predominantly led by 1) expected growth of 9% in earning assets in 1H2012 and, 2) lower provisions. We do not expect any payout with the result. At current levels, we maintain our ‘Hold’ call on the scrip with a target price of Rs122.

NII to remain flat in 2Q on a YoY basis

Net Interest Income (NII) of the bank is likely to remain flat at Rs13.2bn in 2Q2012 on a YoY basis. The same is anticipated to be down by 5% on QoQ basis, mainly on account of revision in the savings deposit rate to 6%. Nevertheless, 1H2012 NII is likely to grow by 3% mainly led by expected growth of 9% in earnings assets during the period.

Non funded income is likely to post a growth of 2%QoQ in 2Q to Rs3.2bn. Rising Fee & Brokerage and income from dealing in foreign currency are anticipated to be key reasons for this growth. In 1H2012, non interest income is likely to be down by 4%YoY due to lower income from dealing in foreign currency (down 40%YoY).

Loan losses to decline by 68%YoY in 2Q

Provisioning on bad loans is likely to settle at Rs732mn in 2Q, down 68%YoY and 43%QoQ. While provision on loans is likely to be on the downside in 2Q, reversal in provision for diminution in investment in 1Q is likely to aid 1H2012 result. Cumulative provisioning expense in 1H2012 is likely to register a decline of 60%YoY to Rs1.93bn.

Operating expenses on the other hand, are anticipated to remain flat at Rs13.5bn in 1H2012, further helping the bottom line.

Investment perspective: ‘Hold’

We currently maintain our ‘Hold’ call on the stock with a target price of Rs122. The scrip currently trades at 2012E PBV and PE of 1.2x and 6.2x, respectively.

+92 (21) 111-574-111 (ext: 3099)

Also in focus

Oil import bill at US$15.2bn in FY12, up 26%YoY

On the back of lower international oil prices, oil imports recorded a decline of 3%MoM in June-2012 to reach US$1.3bn. Subsequently, oil import bill clocked in at US$15.2bn in FY12 vs. US$12.1bn in FY11 (up 26%).

No comments:

Post a Comment